Stablecoins in the Spotlight

Most people have heard of cryptocurrencies, particularly the most well-known one - bitcoin. But cryptocurrencies suffer a major problem with price stability that has left investors with heavy losses.

Stablecoins are meant to provide a solution to the problem of cryptocurrency volatility. Their aim is to mimic traditional currencies, but with the additional benefits of blockchain technology.

Stablecoin popularity has exploded over the past few years. In February, National Australia Bank (NAB) announced that it was creating its own stablecoin - AUDN. The news comes 9 months after ANZ launched 30 million tokens of its own stablecoin tickered A$DC. This article looks at the basics of stablecoins, what is driving their appeal and what they could mean for the future of money.

What are stablecoins?

Stablecoins are digital currencies minted on the blockchain whose value is pegged to a 'stable' underlying asset, such as the US dollar. They operate like any other cryptocurrency, using blockchain to maintain and operate the network, but their value does not flucuate based on supply and demand. Instead, the price remains consistent with the asset it is pegged to, providing a better tool for digital payment transactions.

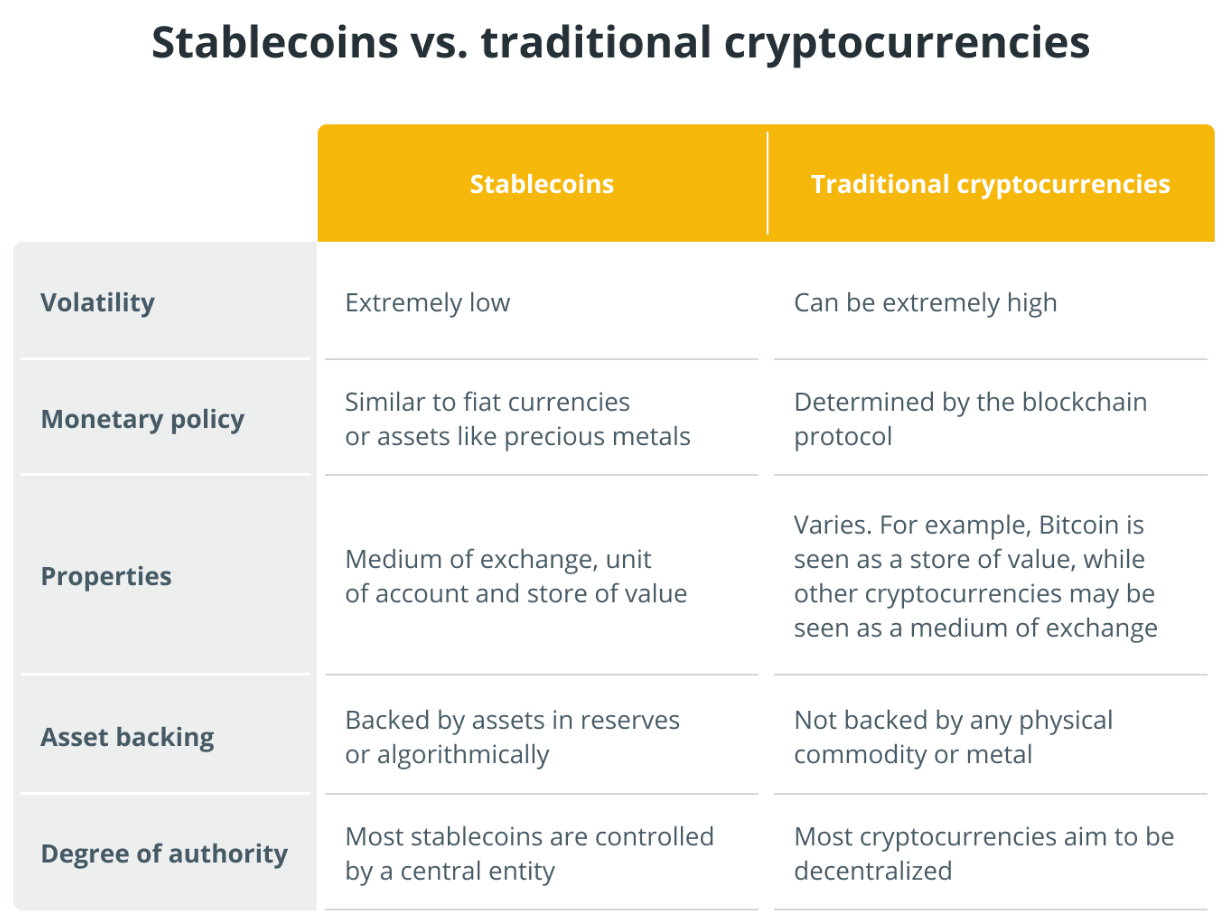

Source: Cointelegraph

Source: Cointelegraph

The Different Flavours of Stablecoins

Stablecoins vary depending on the mechanism being used to support the coin's price. The two most common methods are to maintain a pool of reserve assets as collateral or to use an algorithmic formula to control the supply of the coin.

Collateralised Stablecoins

Collateralised stablecoins maintain a pool of assets to support the coin's value. When the holder of the stablecoin wishes to cash-out their tokens, an equal part is taken out from the reserves. Collateralised stablecoins come in a few forms:

Fiat-backed

The most popular stablecoins are backed 1:1 by a fiat currency. The fiat collateral remains in reserve with a central issuer or a financial institution, and it must remain proportionate to the number of tokens in circulation. USD Coin (USDC) is a prime example of a collateralised stablecoin.

Fully dollar-collateralised stablecoins operate in a similar way to money-market funds, where the peg is backed by a reserve of US Treasuries, certificates of deposit, commercial paper, corporate or municipal bonds. Current issuers include Circle, Gemini, Paxos. The stablecoins issued by ANZ and NAB bank in Australia would fall into this category.

Crypto-backed

Crypto-backed stablecoins are backed by another cryptocurrency as collateral. The process employs a smart-contract instead of relying on a central issuer. When purchasing this kind of stablecoin, you lock you cryptocurrency into a smart contract to obtain tokens of equal representative value. This type of stablecoin is usually over-collateralised to buffer against price fluctuations in the required cryptocurrency collateral asset. DAI is the most prominent stablecoin in this category.

Commodity-backed

Commodity-backed stablecoins are collateralized using physical assets like precious metals, oil, and real estate. The most popular commodity to be collateralized is gold; Tether Gold (XAUT) and Paxos Gold (PAXG) are two of the most liquid gold-backed stablecoins.

Algorithmic Stablecoins

Algorithmic stablecoins maintain their price peg via algorithms that control the supply of the token. This type of stablecoin will reduce the number of tokens in circulation when the market price falls below the fiat currency that it tracks. TerraUSD (UST) was the biggest algorithmic stablecoin, reaching a market cap of more than $18.7 billion at its peak.

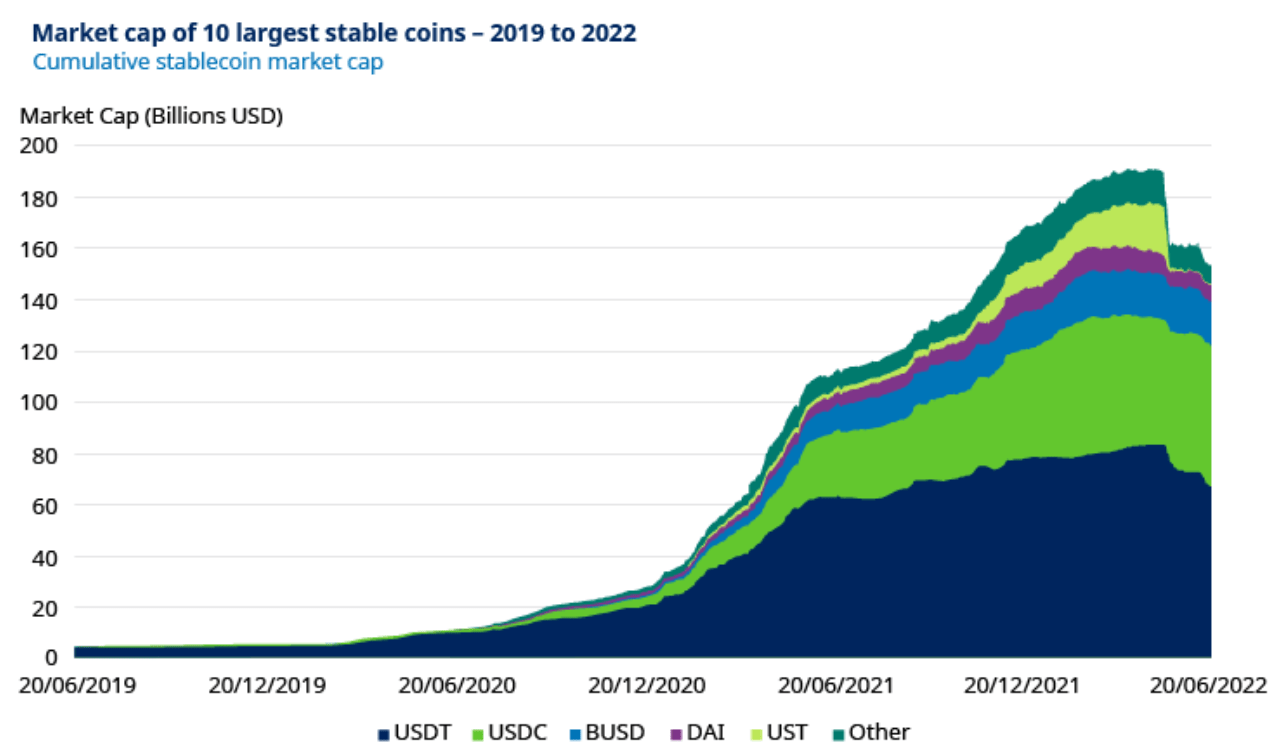

The state of the stablecoin market:

Source: Schorders

Source: Schorders

How are Stablecoins Used?

By bridging the worlds of cryptocurrency and everyday fiat currency, stablecoins have proven to be a useful form of digital money that is better-suited to everything from transferring money between exchanges or day-to-day commerce. Stablecoins bring the benefits of blockchain such as transparency, security, immutability, faster transactions and lower costs, without losing the trust and stability that comes with using a traditional currency. As their popularity has grown, so too has their functionalities within the crypto-asset ecosystem:

- Transfer Money Cheaply

- Trade or Save Assets

- Send Money Internationally

- Minimise Volatility

- Earn Higher Interest

Stablecoins and CBDCs

Most stablecoins are currently minted by private companies, but this will change as central banks are introducing their own, known as CBDCs (central bank digital currencies).

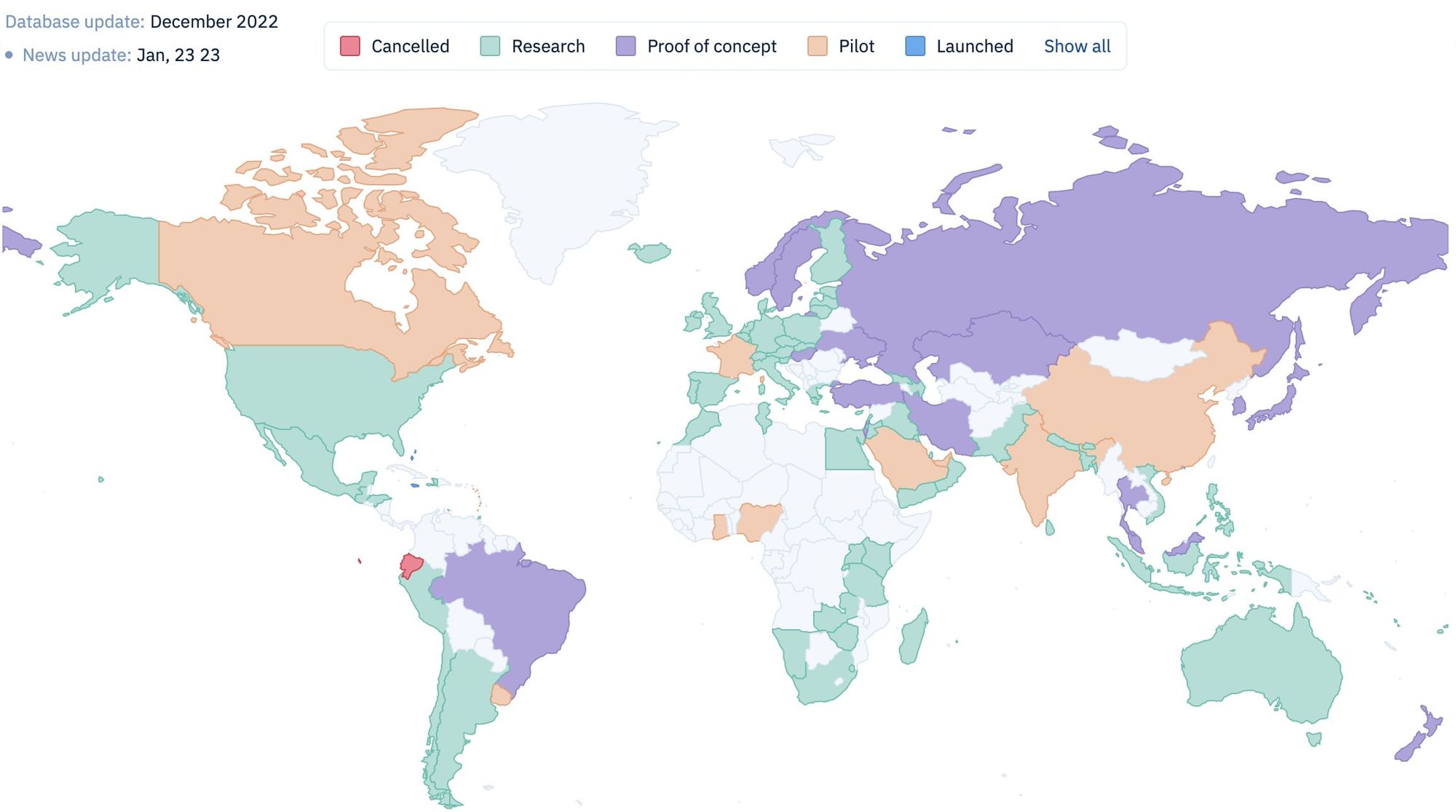

The rapid rise of the number of stablecoins in circulation over the past few years has caused central banks to start exploring their own stable digital currencies in greater earnest. According to McKinsey, over four-fifths of the world's central banks are engaged in pilots or other CBDC activities.

Source: cbdctracker.org

Source: cbdctracker.org

While part of this is likely to due to central bank reservations about privately issued stablecoins on financial stability and traditional money supply, the goal of improving access to central bank money for private citizens is also a factor.

Given how early we are in the process of stablecoin and CBDC co-existence, it's difficult to predict where we will end up. Ultimately, the fate of CBDCs and stablecoins could be decided by the significant forces of regulation and adoption. While CBDCs will be issued under the auspices of central banks, stablecoins are potentially subject to regulatory oversight from multiple agencies, depending on their classification as assets, securities, or even money-market funds.

But there is hope that CBDCs and stablecoins can coexist. In such a world, Mckinsey predicts that we may see flavours like geography, market incumbency by private institutions or by sector. Whatever the outcome, that significant change in digital money is on the horizon is indisputable.